New Bank of England data shows mortgage lending into retirement is now an “entrenched feature” of the market, and is likely to put increase pressure on retirement savings in future.

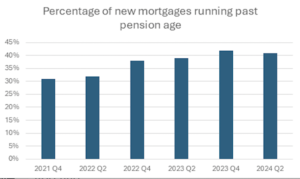

The data, requested by LCP partner Steve Webb, shows that in the second quarter of this year, two in five new mortgages had terms running beyond state pension age. This figures remains high, despite interest rates edging downwards over this period. And this figure is significantly higher than comparative data from the end of 2021.

In total LCP estimates that over a million new mortgages have been issued since the end of 2021 with terms running past pension age. Webb says this has “profound implications” when it comes to retirement planning, particularly with the PLSA’s figures, which quantify how much money is needed to secure a ‘basic’, ‘moderate’ or ‘comfortable’ standard of living in retirement assume that people are not paying housing costs – either in terms of a mortgage or rent.

Webb says this also raises the possibility that people may raid DC pots as they reach retirement to pay off outstanding mortgage debt, potentially making it harder to secure a decent standard of living throughout in their latter years.

LCP data shows the percentage of new mortgages set to run past pension age in alternate quarters from Q4 2021 onwards (see below)

{kind=link}

Pension consultants LCP says that over the last two years (from 2022 to 2024), the growth in new long-term mortgages seems to have happened primarily at younger ages, with a 30 per cent increase in the number of under 40s taking out mortgages that are set to run into retirement.

One of the key reasons for this is affordability, with younger borrowers opting for extended terms in response to high interest rates. However, despite mortgage rates now seeming to be on a downward trajectory, the proportion of new mortgages with these long durations remains at around 2 in 5.

Webb says: “There is increasing evidence that taking out a mortgage which runs past pension age is an entrenched feature of the mortgage market rather than a temporary blip.

“This has profound implications for retirement planning, as it is likely to mean that savers may end up using up already inadequate pension pots to clear a mortgage balance. Anyone involved in helping today’s workers plan for their retirement must now factor in the possibility that housing costs will run into retirement or will have to be funded from already meagre pension pots”.

LCP has compiled a chart showing the percentage of new mortgages set to run past pension age in alternate quarters from Q4 2021 onwards (see below) .