{kind=link}

Six interlocking elements offer a one-stop shop for employers and employees, taking members through accumulation and into retirement, says Platforum senior researcher Miranda Seath

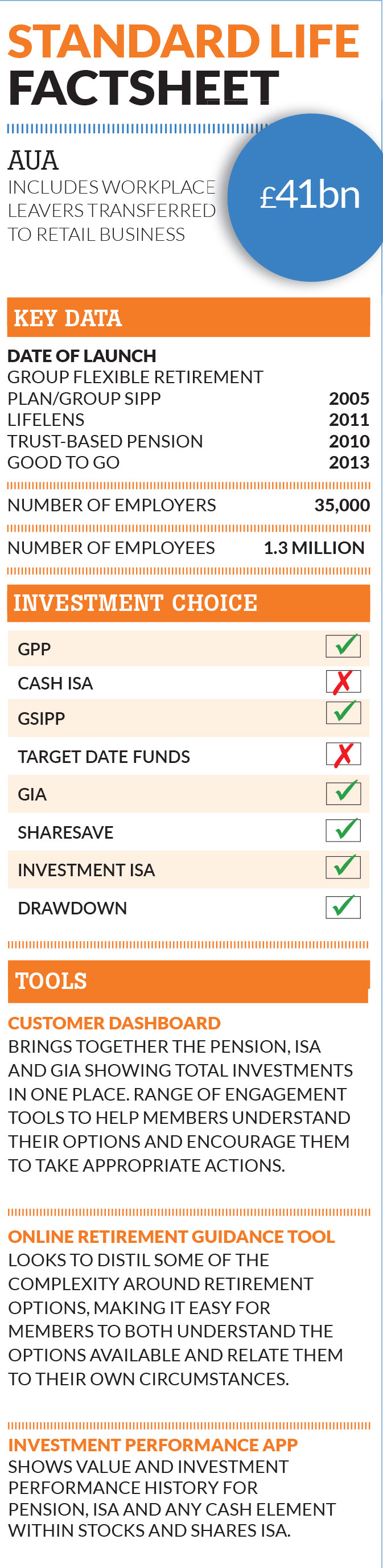

This month we look at Standard Life, the Edinburgh-based firm founded in 1825. Platforum’s research with advisers and employers finds a self-assured workplace pensions and benefits provider that is consistent in approach across the spectrum of employers it works with.

Standard Life sees itself as unique in its ability to cater for firms ranging from micro-employers and SMEs to large schemes across a wide range of industries. It seeks to work with employers that recognise the value of pensions and benefits to their workforce and their business. It says it is focused on the areas that most affect member outcomes: engagement, investment quality and retirement support.

Standard Life is often not the cheapest provider. Its Good To Go proposition for SMEs is typically priced at 75 basis points and employers may be subject to a fee of £100 a month. It is unlikely to be the right choice for those looking just to tick the auto-enrolment box. However, Standard Life argues that its support model will in fact save employers money relative to the cheapest providers.

Vertical integration is at the heart of the proposition. Standard Life head of employer and trustee propositions Alan Ritchie refers to six interlocking elements: pensions and savings products, SLI investment solutions, financial guidance, flexible benefits, communications consultancy and financial advice. As well as helping to meet client and member needs, each rung in the vertically integrated business delivers a greater share of the value chain.

By attracting employers with above-average contributions, Standard Life can funnel good-quality schemes into SLI default funds. These funds, it argues, are designed to offer employees the best retirement outcomes.

At this point in AE staging, Standard Life is still very active in the SME market. The AE mandatory contribution levels are currently low but, when auto-escalation increases contribution rates to 5 per cent in April 2018 and 8 per cent in April 2019, smaller employers will look more attractive for the longer term. By focusing on schemes that encourage higher levels of engagement, the provider is also managing the risk of mass opt-outs.

In our survey, Standard Life scored highly for communication and financial education. Employers with scale can personalise schemes through Lifelens, which powers employee-facing portals for a number of large employers, including National Grid and Telefonica-O2. National Grid prominently displays a window that drives deferred scheme members to Standard Life’s employee zone, where employees can view their investment choices and the value of their pension pot through the portal, and can act online too.

Employee engagement is important for practical reasons. With many members still in funds that target annuity purchase, Standard Life has devised ways of highlighting the option to switch. The Click and Switch initiative is an email, endorsed by the employer, explaining that the employee can switch funds. No log-in is required because the email contains no sensitive information. The employee can make a switch in three clicks. Standard Life tells us that, at one employer, 70 per cent of assets switched for members receiving the email, with the average switching rate around 50 per cent. Once a switch is made, the employee receives a confirmation letter in the post.

Standard Life’s vertically integrated proposition offers a one-stop shop for employers and employees, taking members through accumulation and into retirement. But the provider must walk the line between fostering relationships with advisers and promoting its own services. Ultimately, Standard Life is focused on its promise of ‘happier, healthier, wealthier employees.’ In a time of unprecedented change in pensions, its business looks sustainable.