The last 20 years have seen seismic changes in the relationships between pension providers, advisers and customers. Technology and regulation have both played a big role in this change and we now find ourselves in a period where all parties have to look at their place in the value chain.

A brief history

Twenty years ago, the very first mobile phones were being developed and we lived in a world where the providers were the dominant force in the market place. They developed complex products that only actuaries could really understand and where no matter what happened, the provider would always win.

Ten years ago, we saw the introduction of the iPhone (yes really, there were no apps until then). Advisers gained the upper hand when they were able to play providers against each other to get the best deal. Commission was a factor in scheme placement and employers seemed to be getting all the support they needed at no cost.

Today, technology is so far advanced and we are now seeing increasing use of digital in the pensions industry. The customer is now king – they choose what they will pay for, charges are regulated and commission is dead.

In this new world we are seeing the market tested by different models with employee benefit consultants (EBCs), corporate advisers and providers all trying out different approaches. This is natural evolution for a market that has undergone significant change, and in some cases, the traditional provider/adviser relationship has broken down.

At Scottish Widows, we look across the value chain to offer a tailored and flexible service that can complement different advisers’ offerings and meet customer needs through a modular approach. This is the best way we can see to ensure we remain a partner of choice for many of our corporate introducers, and ensure we’re delivering value for employers and employees.

We are also increasingly seeing employers looking to engage advisers on very specific pieces of work, such as scheme design and selection, and requesting that the provider picks up other parts of the relationship and process.

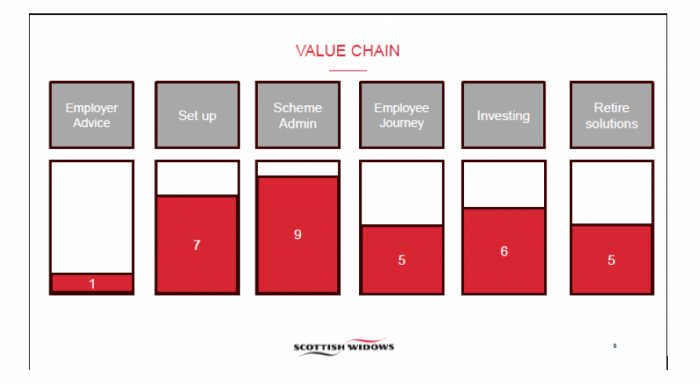

At the recent Corporate Adviser Summit, we asked advisers for their views on which parts of the value chain they wanted to own and which parts they thought providers should be responsible for. Below is a snapshot of the results; the wide variety of responses illustrates just how important a flexible partnership approach is.

A high score means advisers generally prefer the provider to take the lead in providing that service. A low score indicates advisers’ preference to take the lead themselves. This clearly points towards the provider having a significant role to play in running the administration of the scheme, whilst advisers, on average, see their proposition fit into the other key steps in the value chain.

{kind=link}

For example, some employers are happy to pay an adviser to run employee presentations across their sites and provide a view of the pension scheme and other benefits available to employees. However, others would prefer the pension provider to offer this service to their employees – especially if it is included in the price – but it will be limited to talking about the pension.

At Scottish Widows, the number of employee presentations delivered by our team increased by 184% between 2015 and 2016. Demand is so strong, that we are further expanding the team to deliver this service to more customers in 2017 and beyond. But we recognise that any providers offering this service must work closely with advisers to ensure the right schemes are selected and this fits with any wider engagement plans.

The increasing role of digital is significant here – do employees expect to access their pension details through a provider app or an adviser app? In breaking down this part of the journey we got very strong feedback across the board that a provider app is the right place, and we are currently testing these digital services with thousands of employees before fully launching later in the year.

Digital developments have enabled employees to take greater control of their own pension, with really difficult problems of the past – like pension transfers – now solved for many people with a simple non-advised digital journey. Pre-digital, transferring pensions was a process that seemed laborious and scary; the simplification of this process means it can be completed in a fraction of the time, and we are seeing more customers feeling confident and empowered to own this part of the value chain themselves for smaller pots.

In 2017 we expect we’ll continue to see evolution of models but, with the customer remaining king, we truly believe it works best when we sit round the table and flex the value chain to ensure that employers and employees always get best of breed put in front of them.

Robert Cochran is Senior Corporate Pensions Specialist at Scottish Widows.