The Treasury’s plan to introduce a money purchase annual allowance of £4,000 has been accused of penalising members of trust-based schemes and damaging pension freedoms’ ability to help older workers adapt to changing work patterns.

Hargreaves Lansdown’s submission to the Treasury’s consultation on reducing the MPAA calls for the proposed new £4,000 limit to be dropped, and accuses the Government of ‘losing sight of putting individuals first’.

More than 500,000 investors, mainly in their 50s, that have already used the pension freedoms to flexibly access their pension will be immediately caught by the reduced allowance for future pension saving under the Treasury’s proposals.

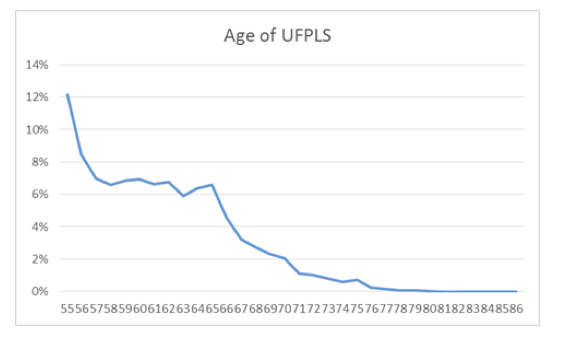

Hargreaves argues members of occupational defined contribution pension schemes written under trust will be placed at a disadvantage as a result of the change because they will not have the option to use drawdown, so will trigger benefits if they draw cash from their pension. Analysis of Hargreaves Lansdown investors who have used the new Uncrystallised Funds Pension Lump Sum (UFPLS) rules shows that a substantial proportion, 41 per cent are under the age of 60; for these investors there is a high likelihood that they will want to make further pension investments in the future.

Pension scheme members contributing over £4,000 will now be hit with unexpected tax charges as a result of the change.

Pension scheme members contributing over £4,000 will now be hit with unexpected tax charges as a result of the change.

Hargreaves Lansdown head of retirement policy Tom McPhail says: “This proposal is symptomatic of a government that has lost sight of the importance of putting individuals first. It is the worst kind of policy-making: it inconveniences and disproportionately penalises millions of ordinary investors and it’s barely going to save the government any money.

“We have searched hard for a solution to the questions posed by the Treasury; we have consulted with industry peers; we have looked at it from every possible angle and in the end our only answer to the Treasury is: ‘Just don’t do it’.

“Nationally we are trying to promote a culture of saving and investing for our future. With the decline of traditional final salary pensions, individuals have to take responsibility for their own retirement. It is up to the pensions industry, employers and the government to help them. This makes it all the more disappointing when you see the government proposing policies which undermine our ability to help investors achieve their goals.”