As the UK defined contribution (DC) market matures, focus is increasingly shifting from accumulation to decumulation, in particular, how members draw down their savings in retirement. Since pension freedoms opened the door to flexible drawdown, more members are choosing to remain invested rather than purchasing an annuity. While this flexibility has many benefits, it has also exposed members to a powerful, but often overlooked danger: sequencing risk.

Sequencing risk refers to the order and timing of investment returns when members begin withdrawing from their pension pots. The sequence of returns has no impact when money is not added to or withdrawn from a portfolio. However, once contributions or withdrawals begin, the sequence of returns starts to matter. If money is withdrawn from a portfolio, two investments may deliver the same annualised return over time yet produce very different outcomes in terms of wealth. A member who experiences negative returns in the early years of withdrawal faces a much higher chance of running out of money compared to another who encounters those same negative returns later in retirement.

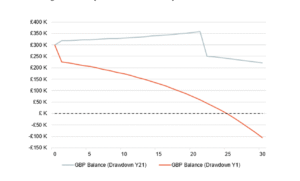

To illustrate, assume two members, each with a portfolio of £300,000 at retirement are withdrawing £18,000 per year. Both portfolios achieve the same annualised return of 5% p.a. over time, with one 25% market “drawdown” occurring at different points in time. All other years deliver identical returns.

{kind=link}

The second member (shown in blue) experiences the same 25% fall, but not until year 21, after a long period of steady returns. Despite both portfolios achieving the same annualised rate of return, the later loss leaves the second member significantly better off, around £327,000 more in value after 30 years. As the chart demonstrates, identical returns in different sequences produce dramatically different outcomes.

Historically, DC defaults have sought to manage sequencing risk by de-risking into bonds and money market funds as members approach retirement. While this approach can help reduce sequencing risk, it introduces new challenges: Safer bonds offer limited returns historically compared to equities; and periods of higher levels of inflation, as experienced since 2021, erode purchasing power and leave members worse off in real terms.

As a result, many DC portfolios entering decumulation are overly conservative, often limiting the potential for long-term growth and making it more difficult for members to sustain withdrawals over a 20 or 30-year retirement.

Sequencing risk starts at the point where withdrawals begin. In accumulation, volatility can be tolerated because losses can be offset by future contributions and time for recovery as no money is withdrawn. However, in decumulation, money is flowing out, not in. A 10% fall in the market is not a 10% loss in value that can be recovered later. Because withdrawals reduce the capital base, the portfolio has less capacity to recover. Negative returns hurt far more during the early years of retirement compared to later years.

Protected Equity Strategies are specifically designed for this type of challenge. They combine traditional equity investments with options (or other derivative overlays) to provide a layer of downside protection while maintaining participation in market gains. Protected equities resolve this dilemma by using hedging to limit severe drawdowns while maintaining meaningful equity exposure. This allows members to hold the higher equity allocations necessary for long-term financial security while mitigating the risk of severe early losses that can be so damaging in decumulation.

A typical protected equity structure may limit annual drawdowns, for example, limiting losses to around 10 to 20 per cent p.a.; reduce volatility to a controlled range, such as 10 per cent p.a.; capture a high proportion of market upside, for example, around 90 per cent of positive market returns and maintain daily liquidity and transparent pricing, features that are essential for DC platforms

The shift from accumulation to drawdown has exposed the limitations of traditional DC investment design. Sequencing risk is often underestimated and often addressed in the wrong way by making portfolios too conservative. Managing it effectively can be one of the most significant determinants of retirement outcomes.

Protected equity strategies offer a pragmatic way forward by keeping members invested in the growth potential of equities while providing a more predictable path through market cycles. In an environment marked by persistent inflation, volatile markets and longer retirements, being invested in equities while reducing drawdown and sequencing risk is essential to achieving the returns necessary to support a long retirement. Protected Equities do not eliminate risk, but they can help members participate more in rising markets while limiting the potential losses during market downturns.

Sequencing risk is the quiet disruptor of DC outcomes. It doesn’t arise from poor long-term performance of the underlying assets, but from bad luck in the timing of returns once withdrawals begin. Protected Equities offer a practical, cost-efficient, and DC-compatible way to address this challenge. By reducing the severity of drawdowns, they can help ensure members’ pots sustain income for longer, turning market volatility from a threat into a managed variable. In today’s DC environment, where retirement outcomes depend as much on stability as on growth, the ability to manage the members’ path of returns may be one of the most valuable tools in the DC decumulation toolkit.