Higher bond yields have pushed down the compensation payments due to those wrongly advised to switch out of DB pensions to record lows.

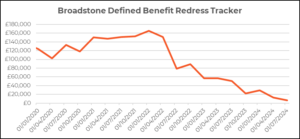

Broadstone’s defined benefit (DB) redress tracker shows that the redress due to a ‘typical’ mis-advised consumer now stands at just £6,600 — radically down from the £150,000 that would have been paid at the start of 2022.

These figures reflect the amount that might be due to an individual, aged 50 who left their DB scheme in 2018, with the scheme promising an inflation-linked pension of £10,000 a year in retirement.

Broadstone says yields have continued to increase through the first half of the year which alongside a modest increase in asset returns has led to a further decrease in the redress payable. This is largely due to the sharp increase in annuity rates, meaning savers can secure a higher level of guaranteed income from their pension pot.

It adds that this minimises the financial disadvantage for those seeking compensation after being wrongly advised to transfer their pension, and therefore the redress they are due.

Broadstone says that redress levels in Q2 2024 broadly halved compared to Q1 when redress for our nominal transferor stood at £12,600. This followed a larger fall in compensation value, with redress of £29,100 due tin Q4 2023.

The DB redress tracker is developed in line with Financial Conduct Authority (FCA) rules for calculating redress with the individual assumed to have invested their funds to earn returns in line with the FTSE Private Investor Index.

Broadstone head of redress solutions Brian Nimmo says: “Yields continued to rise through the first half of the year which, alongside a modest increase in asset returns, has led to a further decrease in the redress payable to our notional consumer. Time will tell as to what the impact of the new government will be on the markets and whether yields will come back in, which would lead to redress increasing again.

“Redress rates can appear volatile given it is calculated as the difference between two large numbers which can move in separate directions making it tricky to second guess how redress will move in individual cases. With this in mind, and especially as the FCA brings in new ‘Polluter Pays’ reforms, it is vital that financial advice firms remain on top of compensation fluctuations to allocate requisite capital against potential claims.”

{kind=link}