{kind=link}

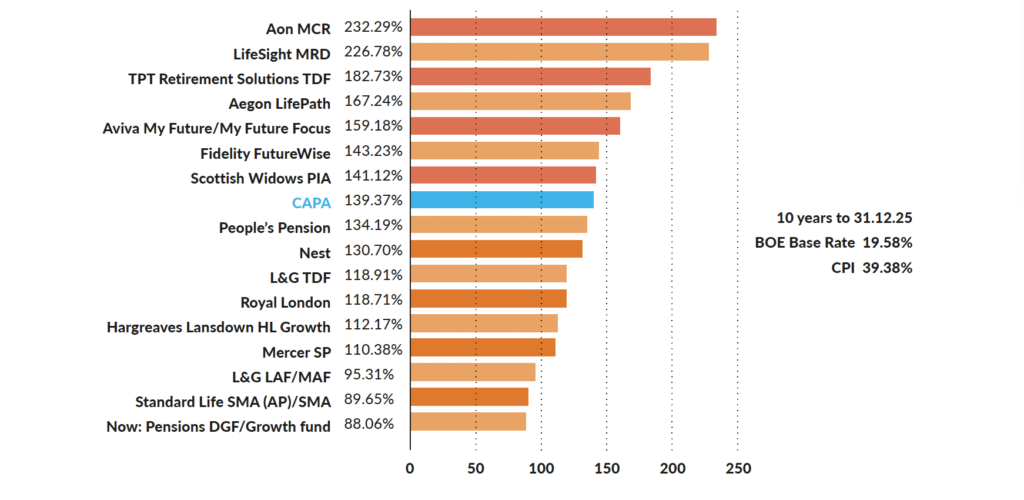

Aon’s default has delivered the highest returns for savers over the past 10 years, with cumulative returns that are almost three times that of Now: Pensions, the worst-performing default over this period.

This is the first time Corporate Adviser’s CAPAdata figures have produced 10 year figures for DC multi-employer workplace pensions. These figures, which relate to savers in the growth phase, show the range of outcomes between the best and worst performers.

The graph pictured compares the cumulative percentage returns for the main defaults of all leading DC workplace pension providers over a 10 year period to (to 31.12.2025).

In total, Aon’s Managed Core default delivered a return of over 232 per cent over this 10 year period. This equates to an annualised rate of 12.76 per cent, after charges. In contrast savers in Now: Pensions default fund achieved a return of just 88 per cent over the same period, giving an annualised return of 6.52 per cent.

Both figures assume a typical 0.5 per cent charge deducted from the annualised return, and relate to the growth phase of the default, for those 30 years from state pension age.

LifeSight, the master trust run by WTW delivered the second highest return over the 10 years, with its MRD default delivering cumulative return of 226.78 per cent. This was followed by TPT Retirement Solutions, whose TDF default delivered 182.73 per cent and Aegon, whose LifePath default delivered 167.24 per cent.

Many of the biggest names in the pensions industry have delivered below average figures over this 10 year period. Standard Life has delivered a cumulative return of just 89.65 per cent on its largest default, in terms of active members, while L&G has delivered 95.31 per cent (for its LAF and MAF defaults) — both only just ahead of Now: Pensions.

Both Standard Life and L&G have launched new defaults over this period, but the CAPAdata chainlinks these defaults in order to show the returns delivered for the majority of active savers. The government proposes using the same system for its new Value for Money metrics.

Other providers to have delivered below average returns include Aviva (on its MFF default), Royal London, L&G (for its TDF default), People’s Pension and Nest.

The CAPA average shows cumulative return of 139.37 per cent over this 10 year period.

A number of providers including Now: Pensions and L&G have revamped their investment strategies for their main defaults and this has led to improved performance over more recent timescales.

All providers that have a 10 year track record have delivered returns that more than double the rate of CPI inflation, and all but three have more than doubled members’ pots in this period.

These figures show how higher annual investment returns compound to significantly higher cumulative figures over longer periods of time. While the Aon annualised return rate is almost double the Now: Pensions annualised return, the Aon 10-year cumulative return is approaching three times the cumulative return of the Now: Pensions fund.

Were the return differentials to continue over 30 years, £10,000 in the 6.52 per cent annualised return fund would grow to just over £70,000. The same amount in the 12.76 per cent annualised return fund would grow to over £450,000.

This data comes ahead of the new Value for Money framework, which will requires providers to publish information on past performance. This follows the CAPAdata example, where schemes will be provided to publish data for savers 30 years from SPA, five years from SPA and at-retirement.

Full details of fund performance, as well as asset allocations will be published in Corporate Adviser’s Master Trust and GPP report, which will be published later this month.