The UK’s fast-maturing defined benefit (DB) market has seen a decline in total fiduciary mandates assets remaining flat for the first time since 2008, according to research from Isio.

Buy-ins more than doubled year-on-year, with 48 per cent of mandate reductions linked to insurance transactions.

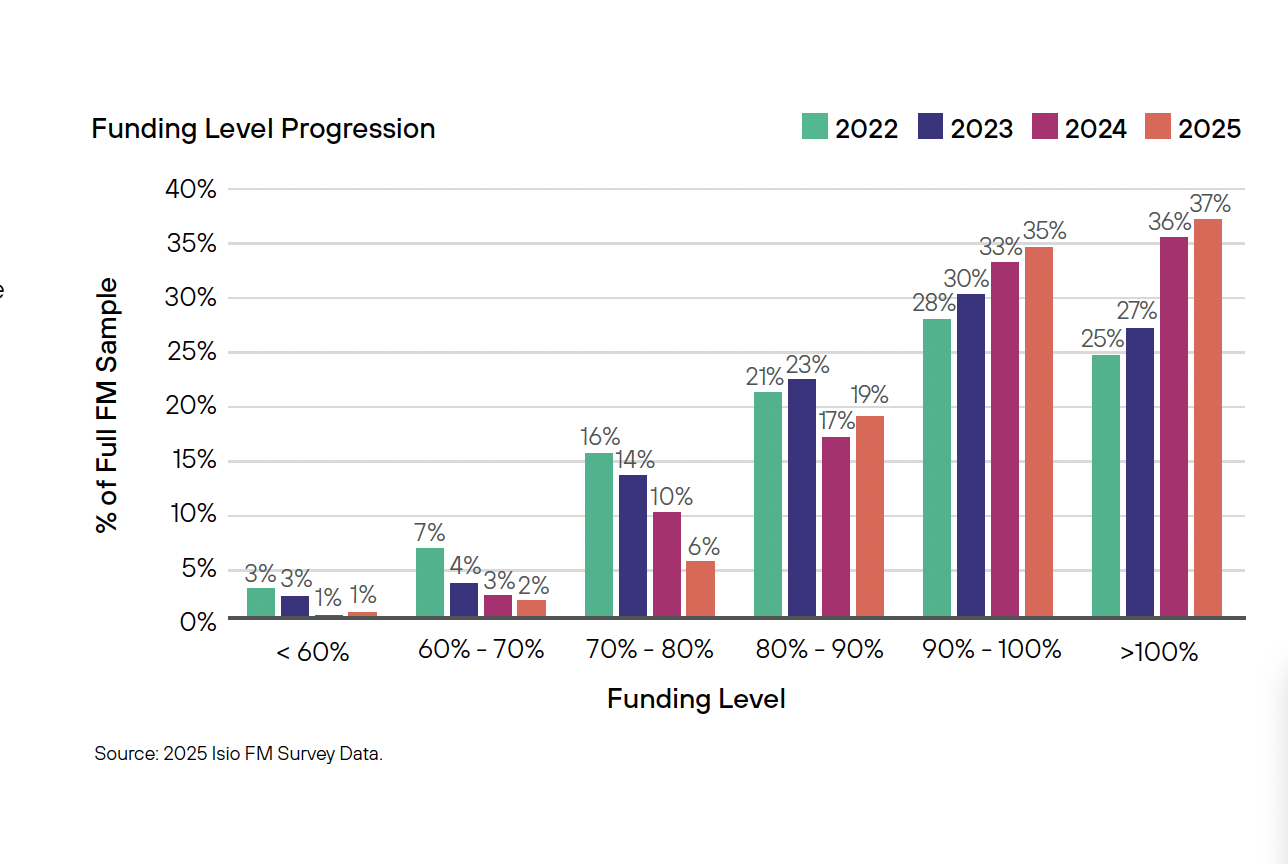

The research finds 72 per cent of fiduciary management mandates have funding levels above 90 per cent, and 37 per cent are fully funded – a 44 per cent increase in three years.

The UK’s fiduciary management market has entered a new phase of maturity and strategic importance as it supports more defined benefit (“DB”) pension schemes towards their endgame. Says Isio’s Latest Fiduciary Management Survey. The survey shows that insurance transactions – particularly buy-ins – among schemes run by fiduciary managers have surged in 2025, more than doubling year-on-year to capitalise on improved funding positions and favourable pricing conditions.

Despite the rapid shift toward insurance, overall fiduciary market activity remains robust. Total assets under management remain broadly the same at £241bn in 2025, compared to £242bn in 2024, while total mandates have decreased by 4 per cent, down from 865 in 2024 to 832 in 2025.

Over 60 new mandates were awarded over the 12 months to 30 June 2025 – largely through full delegation – while partial-mandate assets managed increased by 4 per cent, from £65bn up to £68bn. Large Outsourced Chief Investment Officer (“OCIO”) arrangements continued to expand and now account for 53 per cent of total fiduciary assets in the UK defined benefit fiduciary management market, helping offset the impact of scheme exits following insurance transactions.

Half of schemes (50 per cent) are targeting insurance-based long-term objectives, reflecting an industry-wide pivot towards risk transfer, says the report. The volume of buy-ins has more than doubled from 13 in 2024 to 30 in 2025, while the number of buyouts remained broadly stable. Almost half the reduction in FM mandates over the past year are directly attributable to insurance transactions.

Alongside this, run-on strategies are gaining momentum as schemes with surpluses choose to retain control of assets and manage them for long-term value. Fiduciary managers are responding with cashflow-driven investment (“CDI”) solutions and flexible growth strategies that balance liquidity with return potential.

As schemes mature and funding levels improve, fiduciary portfolios are becoming simpler, more liquid and more cost-efficient. On average, equity allocations have increased by around 4 per cent to 23 per cent compared with 2024, the largest equity allocation we have observed in recent years, while allocations to illiquid assets have fallen by approximately 2 per cent. Fiduciary managers continue to favour traditional growth assets supported by derivative strategies that mitigate downside risk without compromising liquidity, says Isio.

The use of active management has declined year-on-year, reflecting cost discipline and a reduced appetite for complex, higher-fee approaches. More than half (58 per cent) of mandates now target returns of liabilities +1.5 per cent per annum or below – a sign of a market focused on low-risk portfolios that support insurance or run-on outcomes.

Paula Champion, partner and head of fiduciary management oversight, Isio, says: “This is the first time we have not seen major fiduciary mandate and asset growth since 2008, reflecting the higher numbers of defined benefit schemes taking advantage of improved funding positions and the greater variety of endgame options available to them. Despite this trend, the fiduciary management market has proven remarkably resilient, through a notable expansion of partial and OCIO mandates.

“Fiduciary managers are playing integral roles supporting defined benefit schemes in their journeys towards their endgame. Their importance can be seen in the combination of a sharp rise in insurance transactions and flat year-on-year numbers for total fiduciary management assets and a marginal reduction in mandates.

“Fiduciary managers are responding to more schemes accelerating their endgame plans by focusing on insurer-ready portfolios, cost-efficient structures and governance frameworks that deliver clarity and control. They continue to demonstrate true value, helping schemes complete their endgame confidently while safeguarding member outcomes. For many trustees who choose to delegate their investment decision-making, a fiduciary approach can provide a high standard of portfolio management and governance for schemes targeting run-on.”

{kind=link}